The COVID-19 pandemic takes a toll on the insurance sector, especially in areas like life, health, travel, events, and trade credit. Insurers offered discounts to support their clients since the lockdown, employment, and other issues caused by the coronavirus epidemic reduced their spending power. Market volatility and reduced customer confidence are other factors that will influence the insurance sector during the COVID-19 pandemic and a long time after this passes.

Here are a few facts and figures that offer a perspective of the challenges faced by the insurance sector during the COVID-19 pandemic, according to the 2020 OECD Global Insurance Market Trends report:

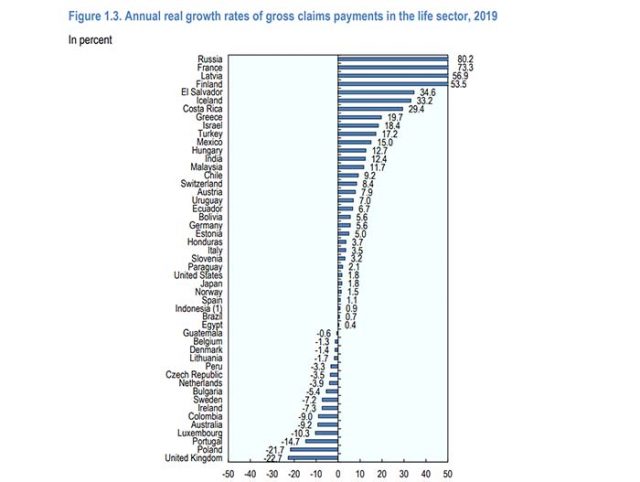

- Data for 2019 revealed that insurance companies experienced an increase in their gross claims payments for life insurance. Some of the most affected markets include: Russia (80.2%), France (73.3%), Latvia (56.9%), Finland (53.5%), El Salvador (34.6%), Iceland (33.2%), Costa Rica (29.4%), and Malaysia (11.7%).

- Other countries experienced declines in gross claims payments for life mainly due to a decrease in surrenders, among them: the United Kingdom (-22.7%), Poland (- 21.7%), and Portugal (-14.7%).

- Gross claims payments increased in the non-life sector in most countries: Luxembourg (100%), Ireland (29.8%), Belgium (26.5%), Latvia (25.4%), and Egypt (25.2%), among others.

- Other countries experienced declines in gross claims payments for non-life insurance. Among them: El Salvador (-17.6%), Honduras (-11.6%), and Ecuador (-10.6%).

The realities of the new normal impacted the insurance sector and triggered several trends and innovations in their digital operations.

Digital Trends and Innovations for the Insurance Sector During the COVID-19 Pandemic

The need for personalization pushes insurance companies to increase their innovation efforts, pushing beyond traditional coverage to enhance the customer experience digitally.

InsurTech

InsurTech companies use digital technologies to offer benefits and lower costs for insurers and their customers. About 14.5 billion U.S. dollars were invested in global Insurtech companies in 2020, and the number may grow in 2021, but the data is not in yet.

InsurTech companies leverage big data, AI, and other technologies to improve the customer experience by making coverage more accessible and faster coverage issuance. At the same time, insurers benefit from lower costs and improved operations.

Artificial Intelligence (AI)

Artificial Intelligence (AI) is a trend influencing all business sectors. AI-enabled software, wearables, voice-assisted devices, connected appliances, and other applications shape consumer expectations more and more. For example, insurance companies adopted AI-powered tech to satisfy these expectations and leverage data to improve the customer experience.

Insurers can use AI to monitor social media data and understand customer sentiment about coverage, customer service, and expectations. This type of information allows insurers to customize policies to address the population’s changing needs and personalize their offers. Improved operations is a direct result of employing AI data, too: it could help to predict and manage fraudulent claims, expenses, losses, settlements, and litigation.

IoT Technology

IoT technology helps insurers to optimize and personalize their offerings to attract more customers with better premiums and services they need instead of generic coverage that doesn’t always apply to their situations.

An example of innovation in the field comes from Beam Dental, a company offering dental benefits by incorporating dental hygiene behavior into policy pricing. Members receive a Beam toothbrush and paste, which connects to a free app that tracks and helps users improve their brushing habits.

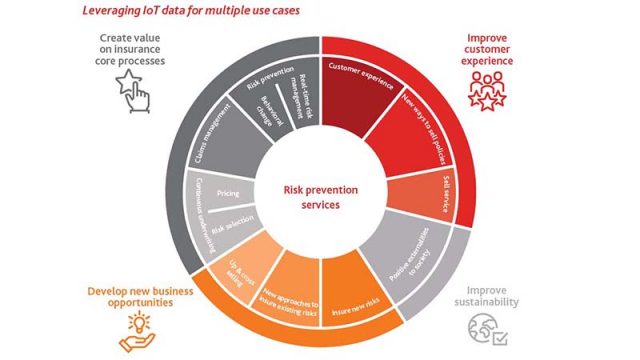

IoT has many other benefits for insurers and insured alike: risk prevention, real-time risk management, continuous underwriting, insure new risks, and so on:

Source Matteo Carbone, director of the IoT Insurance Observatory

To put things in perspective, the global Internet of Things (IoT) insurance market is likely to reach US$265.6 billion by 2026, compared to US$15.1 billion in 2020.

Chatbots

Chatbots are not new, but many insurance companies lagged behind adoption before COVID-19. However, now companies understand the advantages these AI-powered solutions offer for customer service and reducing the workload on staff.

Chatbots can easily address FAQs, and they are available 24/7. They are also helpful in assisting clients with claims or other service requests, putting them in contact with a human representative when needed, collecting customer data, pushing special offers, sending renewal notifications, and so on.

For example, the insurance division customer support for Yellow.ai brought in $100 million in three years, the company said.

Takeaway

The insurance sector must continue to adapt and innovate to recover from the losses caused by the COVID-19 pandemic and satisfy emerging customer demands and expectations. While new technologies may seem costly, the future is digital, and the global power players in the sector are already ahead of the curve. AI, IoT, and other technologies raise operational efficiency and help find new business models and better products for their clients.