This article is the first in a series of 12 articles, based on comprehensive research into Direct Bookings Growth Strategy conducted by Schieber Research and Carmelon Digital Marketing. Each article in the series takes a deep dive into one of the report's key chapters.

The hospitality industry is at a turning point, one that's been building for years and is now impossible to ignore. For two decades, online travel agencies were the default. Guests used them because they were convenient. Hotels accepted them because the volume was there. And somewhere along the way, the industry handed over guest data, margin, and the direct relationship with its own customers, one commission at a time.

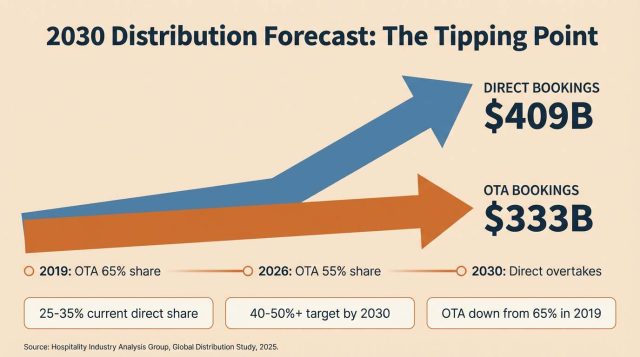

But the numbers are shifting. New research from Skift and SiteMinder, analyzed here by Carmelon Digital Marketing and Schieber Research, shows that by 2030, direct digital bookings will reach $409 billion overtaking OTAs, which are projected at $333 billion. That's not a forecast about some distant future. It's a reversal of the distribution structure that has defined this industry since the internet changed travel forever.

For CMOs, VP Revenue, and distribution leaders, this isn't a trends piece. It's a practical look at where the market is heading, what the top performers are doing differently, and what that means for the decisions you're making right now.

The Profitability Equation: $519 vs. $320

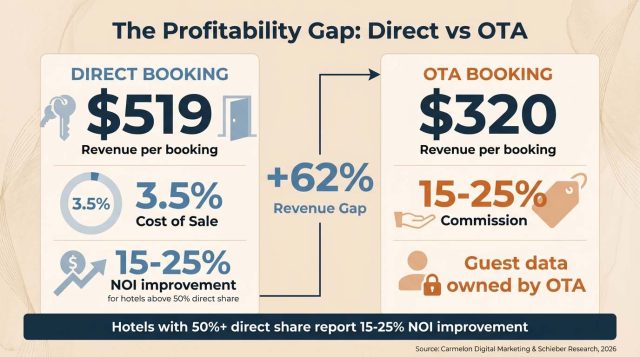

Let's start with the number that should be on every Revenue meeting agenda. The average direct booking generates $519 in revenue. The average OTA booking generates $320. That's a 62% gap before commissions even enter the picture.

On the cost side, running a direct channel costs around 3.5% of revenue. OTA commissions run 15–25%. When you put those two things together, the math becomes hard to argue with. Hotels that have pushed their direct booking share above 50% are reporting 15–25% improvement in NOI, that's Net Operating Income, meaning revenue after operating costs are taken out, before tax and debt. Direct bookings also tend to come with longer stays and, crucially, full ownership of guest data, something that only becomes more valuable as AI and personalization become central to distribution.

The research puts it simply: this isn't a marketing problem. It's a product and profitability problem.

February 2025: The End of Risk-Free Advertising

There's one change that some marketing managers still haven't fully absorbed. In February 2025, Google shut down its commission-based bidding model for hotel ads, Pay-Per-Stay and Pay-Per-Conversion, which had let hotels advertise on metasearch and only pay when a booking was actually completed. That safety net is gone.

The new model runs on CPC (cost per click - you pay every time someone clicks your ad, regardless of whether they book) and ROAS (Return on Ad Spend - how much revenue you're generating for every dollar spent on advertising). The risk now sits entirely with the hotel.

Here's why that matters day to day: if your direct rate appears higher than the OTA rate on Google, because of a wholesaler leak, a distribution inconsistency, or anything else - the guest clicks the OTA link. You paid for the impression. You lost the booking.

Rate Parity - keeping your price consistent across all channels - has gone from best practice to basic operational hygiene. Tools like RateParity and OTA Insight aren't optional extras. They're table stakes. Hotels running well-optimized metasearch campaigns are seeing ROAS of 3–5x, with the best performers hitting 10x.

At the same time, regulation in Europe is shifting the rules in the other direction. The DMA - Digital Markets Act designates Booking.com as a "Gatekeeper" and prohibits it from enforcing rate parity clauses. The practical implication for hotels operating in European markets: you can now legally price your direct channel lower than the OTA, without fear of algorithmic retaliation.

Two Models That Are Actually Working

The research identifies two distinct paths to high direct booking share. They're different in approach, but both have real results behind them.

The first is the "Walled Garden" model, the approach taken by the major enterprise chains. Marriott, Hilton, and IHG have spent decades building loyalty ecosystems that are genuinely hard to replicate. With over 210 million loyalty members, co-branded credit cards, and deep airline partnerships, these brands generate 50–60% of their occupancy through loyalty programs alone. Their direct channel isn't just a website, it's a fully integrated ecosystem.

The second model belongs to Mid-Scale chains, and the clearest example is Premier Inn. With over 900 hotels, the British chain achieves more than 99% direct bookings in its domestic market, and it got there through one straightforward decision: staying off the major OTAs entirely. The foundation is brand consistency, a clear value proposition, and an offer that guests can only access by booking directly.

The Premier Inn "Book Direct" campaign in the Middle East brought that logic to life: +262% in booking revenue, +46% in direct website bookings, +124% in organic search revenue. The strategy wasn't complicated. Same price as the OTA, plus exclusive perks: early check-in, late checkout, F&B discounts. Guests chose direct not because it was cheaper, but because it was better.

Attribute-Based Selling: The Smarter Way to Fence Value

One question that comes up constantly in direct booking conversations is how to make the direct channel more attractive without technically breaking Rate Parity. The answer that's gaining real traction - both in this research and among leading hotel groups, is Attribute-Based Selling, or ABS.

The concept is simple. Instead of selling a "standard room" across every channel, your direct site offers something more specific, high floor, away from the elevator, sea view, early spa access. The OTA lists a standard room. Your site lists a different product entirely, one that price-comparison tools can't match against. The fence is built into what you're selling, not what you're charging.

On top of that, Member-Only Rates, pricing that lives behind a login and is invisible to OTA algorithms, Geo-Fenced offers based on where the guest is searching from, and private pricing through direct email all give hotels ways to compete on value without starting a price war.

Gen Z Isn't Using Google

This shift is running in parallel with something happening in how younger travelers search, and it has real budget implications. Around 40% of Gen Z use TikTok and Instagram as their primary tool for travel research. Not just for travel inspiration - as the actual starting point of the booking process. 33% of TikTok users booked a trip within six months of watching travel content on the platform.

In September 2025, TikTok launched Travel Ads, a travel-specific ad format that shows hotel names, prices, and ratings with the ability to book directly inside the app. Accor was the first hotel group to test it at global scale. The results: 46% lower cost-per-booking (CPB) and ROAS (Return on Ad Spend) that was 2.3x higher than other channels. TikTok took it a step further in 2025 with a direct partnership with Booking.com, testing in-app hotel bookings for U.S. users, so a traveler inspired by a video could complete a booking without ever leaving TikTok.

For a sense of where this is going, look at China. Douyin- TikTok's Chinese equivalent, recorded $40 billion in travel bookings in 2024, with over 100,000 hotels on the platform. The Western market is a few years behind that. Not many.

AI-to-AI: When the Booking Happens Without a Human

The biggest distribution shift coming by 2030 isn’t about a new channel. It’s about who makes the booking. In January 2026, Google introduced UCP - the Universal Commerce Protocol - an open standard designed to let AI agents on Google surfaces, including Gemini and Google AI Mode, complete transactions directly. OpenAI is building a parallel path through its Agentic Commerce Protocol for ChatGPT. For hotels, the direction is clear: AI agents may soon be able to complete an entire hotel booking directly with the property. No OTA. No traditional website visit. The hotel stays as Merchant of Record and keeps full ownership of guest data.

UCP works alongside MCP - Model Context Protocol (a protocol that allows AI agents to read and use information from external systems), Agent2Agent, and Agent Payments Protocol. It was co-developed with Shopify, Target, and Walmart, and is backed by Visa, Mastercard, Stripe, and over 20 industry partners. This isn't a concept. It's live infrastructure.

The practical implication is straightforward. Hotels that don't build open API (Application Programming Interface, the technical connection that lets different systems talk to each other) infrastructure will end up as inventory inside an OTA's AI system. The same dependency that exists today, just on a newer platform. The core investment to avoid that is a CDP - Customer Data Platform (a system that pulls all guest data from different sources into one unified profile) that feeds all AI systems, alongside a dynamic pricing engine. Research shows that combination can deliver RevPAR (Revenue Per Available Room - the standard metric for hotel pricing performance) improvements of 15–30% in year one.

What Marketing Managers Need to Actually Do

Data doesn't move a distribution strategy on its own. Here are the five things every marketing and revenue leader needs to have on their radar:

Make sure Rate Parity is being monitored continuously. In a pay-per-click metasearch world, one rate leak from a wholesaler can waste an entire media budget and hand the booking to a competitor. This isn't a tech team issue - it's a management accountability issue.

Put the real budget behind social and TikTok. Gen Z is not on Google. If your media spend is still weighted almost entirely toward paid search and metasearch, there's a widening gap between where you're investing and where your future guests actually are.

Build a simple loyalty club with immediate value. Not a tiered points program with a two-year redemption window. A "sign up and save" club that gives guests something tangible the moment they register. The real goal is the email address, and the start of a direct relationship you actually own.

Decide which room attributes are direct-only. ABS doesn't require a new tech platform. It requires a decision: which features - floor level, view, quiet location, are exclusively available to guests who book directly. That's how you create real value differentiation without touching your pricing agreements.

Plan your data infrastructure now. A CDP isn't a luxury, it's the foundation for personalization, smart pricing, and everything AI-related in distribution. Most hotels already have the data. It's just sitting in separate systems. The work is connecting it before the market gets too far ahead.

The Bottom Line

The data is clear. The direction is clear. And the window is open, but not indefinitely.

The hotels winning this shift didn't get there all at once. They built the foundation over time: collected guest data, created an offer that guests can't find on Booking.com, and stopped treating their website as just another digital asset. They made the direct channel the flagship product of the business.

By 2030, the gap between a hotel that built its direct channel and one that kept relying on OTAs won't just show up in commission costs. It'll show up in data, in loyalty, in pricing capability, and in the ability to have a real relationship with guests without a third party sitting in the middle.

The question isn't whether to invest directly. It's how much longer you can afford not to.

This article is part one of an ongoing series based on the Direct Bookings Growth Strategy research by Schieber Research and Carmelon Digital Marketing, with each article focusing on one of the report's key themes. Data and statistics referenced throughout are sourced from third-party research providers, primarily Skift and SiteMinder, alongside additional industry sources.